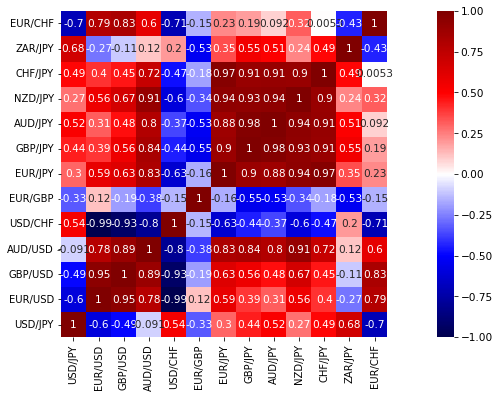

クロス円の値動きを見ていると、USDJPYに引かれているのかドルストレートに引かれているのか、数値的に解釈するために、各通貨間の相関係数を計算するコードを作成した。

from datetime import datetime

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

import numpy as np

import yfinance as yf

from statsmodels.tsa.stattools import adfuller

import plotly.express as px

USDJPY = "USDJPY=X"

EURUSD = "EURUSD=X"

GBPUSD = "GBPUSD=X"

AUDUSD = "AUDUSD=X"

USDCHF = "USDCHF=X"

EURGBP = "EURGBP=X"

EURJPY = "EURJPY=X"

GBPJPY = "GBPJPY=X"

AUDJPY = "AUDJPY=X"

NZDJPY = "NZDJPY=X"

CHFJPY = "CHFJPY=X"

ZARJPY = "ZARJPY=X"

EURCHF = "EURCHF=X"

START_DAY = "2023-01-01"

END_DAY = "2023-01-11"

usdjpy = yf.download(USDJPY, start=START_DAY,end=END_DAY)

eurusd = yf.download(EURUSD, start=START_DAY,end=END_DAY)

gbpusd = yf.download(GBPUSD, start=START_DAY,end=END_DAY)

audusd = yf.download(AUDUSD, start=START_DAY,end=END_DAY)

usdchf = yf.download(USDCHF, start=START_DAY,end=END_DAY)

eurgbp = yf.download(EURGBP, start=START_DAY,end=END_DAY)

eurjpy = yf.download(EURJPY, start=START_DAY,end=END_DAY)

gbpjpy = yf.download(GBPJPY, start=START_DAY,end=END_DAY)

audjpy = yf.download(AUDJPY, start=START_DAY,end=END_DAY)

nzdjpy = yf.download(NZDJPY, start=START_DAY,end=END_DAY)

chfjpy = yf.download(CHFJPY, start=START_DAY,end=END_DAY)

zarjpy = yf.download(ZARJPY, start=START_DAY,end=END_DAY)

eurchf = yf.download(EURCHF, start=START_DAY,end=END_DAY)

alldata = pd.concat([usdjpy.Close,eurusd.Close,gbpusd.Close,audusd.Close,

usdchf.Close,eurgbp.Close,eurjpy.Close,gbpjpy.Close,

audjpy.Close,nzdjpy.Close,chfjpy.Close,zarjpy.Close,

eurchf.Close],axis=1)

alldata.columns = ('USD/JPY','EUR/USD','GBP/USD','AUD/USD',

'USD/CHF','EUR/GBP','EUR/JPY','GBP/JPY',

'AUD/JPY','NZD/JPY','CHF/JPY','ZAR/JPY',

'EUR/CHF')

alldata.dropna()

correlation_coefficients = alldata.corr()

fig,ax = plt.subplots(figsize=(18,6))

plt.rcParams['font.size'] = 10.5

plt.rcParams["figure.figsize"] = (20,3)

sns.heatmap(correlation_coefficients, vmax=1, vmin=-1, cmap='seismic',

square=True, annot=True, xticklabels=1, yticklabels=1)

plt.xlim([0, correlation_coefficients.shape[0]])

plt.ylim([0, correlation_coefficients.shape[0]])

plt.show()

2023年の最初から現在までのdataを解析すると、クロス円はUSDJPYよりもドルストレートの値動きに引きずられていると考えられる。