引き続きUdemyでPython for Time Series Data Analysisの学習を進めている。Pandasを用いたTime Series Dataの解析手法に関する内容。

Datetime classの使用例

from datetime import datetime

my_year = 20

my_month = 1

my_day = 2

my_hour = 13

my_min = 30

my_sec = 15

my_date = datetime(my_year,my_month,my_day)

my_date

my_date_time = datetime(my_year,my_month,my_day,my_hour,my_min,my_sec)

type(my_date_time)

my_date_time.hour

np.array(['2020-03-15','2020-03-16','2020-03-17'],dtype='datetime64[h]')

np.arange('1968','1976',dtype='datetime64[D]')

index methodの使用例

import pandas as pd

pd.date_range('Jan 01, 2018',periods=7,freq='D')

pd.to_datetime(['1/2/2018','Jan 03, 2017'])

pd.to_datetime(['2/1/2018','3/1/2018'],format='%d/%m/%Y')

data = np.random.randn(3,2)

cols = ['A','B']

print(data)

idx = pd.date_range('2020-01-01',periods=3,freq='D')

df = pd.DataFrame(data,index=idx,columns=cols)

df

df.index

df.index.max()

df.index.argmax()

df.index.min()

df.index.argmin()

resample methodの使用例

import pandas as pd

df = pd.read_csv('./UDEMY_TSA_FINAL/Data/starbucks.csv',index_col='Date',parse_dates=True)

df.head()

df.index

df.resample(rule='A').mean()

def first_day(entry):

if len(entry) != 0:

return entry[0]

df.resample(rule='A').apply(first_day)

df.head()

df['Close'].resample('A').mean().plot.bar()

shiftメソッドの使い方

import pandas as pd

df = pd.read_csv('./UDEMY_TSA_FINAL/Data/Starbucks.csv',parse_dates=True)

df.head()

df.tail()

df.shift(1).tail()

df.shift(-1).tail()

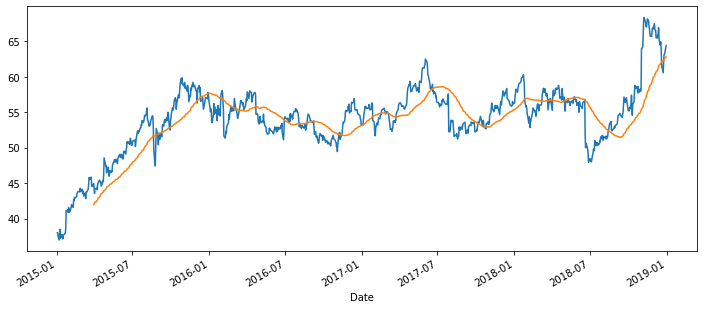

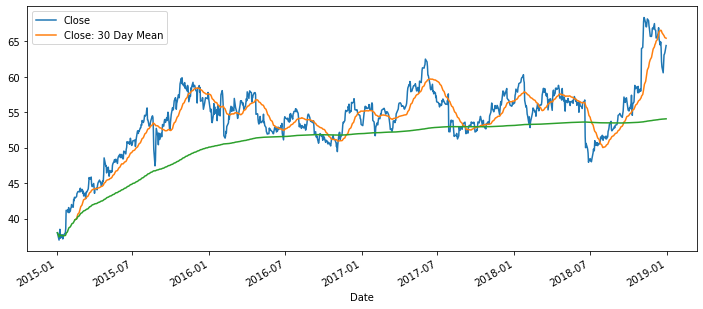

rollingを用いた移動平均線のplot

import pandas as pd

df = pd.read_csv('./UDEMY_TSA_FINAL/Data/Starbucks.csv',index_col='Date',parse_dates=True)

df.head()

df['Close'].plot(figsize=(12,5))

df.rolling(window=60).mean()['Close'].plot()

df['Close: 30 Day Mean'] = df['Close'].rolling(window=30).mean()

df.head

df[['Close','Close: 30 Day Mean']].plot(figsize=(12,5))

df['Close'].expanding().mean().plot(figsize=(12,5))

plotの整形

import pandas as pd

df = pd.read_csv('./UDEMY_TSA_FINAL/Data/starbucks.csv',index_col='Date',parse_dates=True)

df.head()

df.index

df['Close'].plot()

df['Volume'].plot()

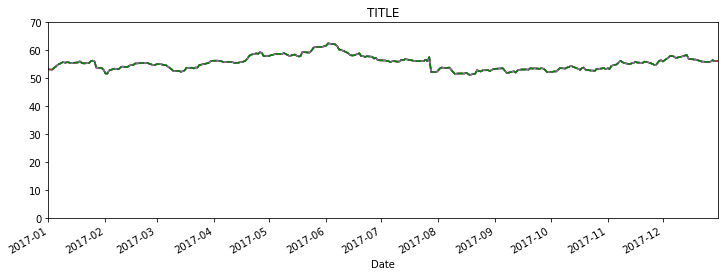

title = 'TITLE'

ylabel = 'Y LABEL'

xlabel = 'X LABEL'

df['Close'].plot(figsize=(12,6),title=title)

ax.autoscale(axis='both',tight=True)

ax.set(xlabel=xlabel,ylabel=ylabel)

df['Close'].plot(figsize=(12,4))

df['Close']['2017-01-01':'2017-12-31'].plot(figsize=(12,4),xlim=['2017-01-01','2017-12-31'])

df['Close']['2017-01-01':'2017-12-31'].plot(figsize=(12,4),ylim=[0,70],ls='--',c='green')

Plotの整形

from matplotlib import dates

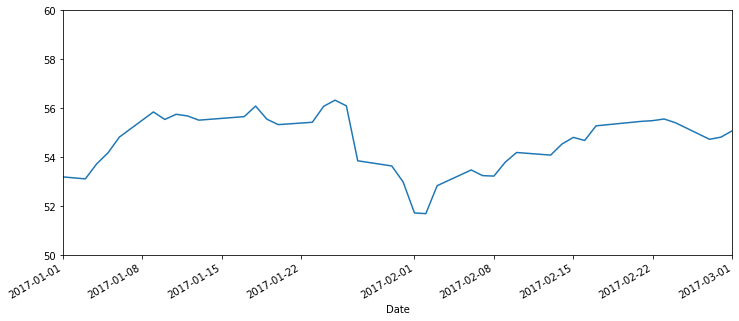

df['Close'].plot(xlim=['2017-01-01','2017-03-01'],ylim=[50,60],figsize=(12,5))

ax.set(xlabel='')

ax.xaxis.set_major_locator(dates.WeekdayLocator(byweekday=0))

ax.xaxis.set_major_formatter(dates.DateFormatter('%a-%B-%d'))

ax.xaxis.set_minor_locator(dates.MonthLocator())

ax.xaxis.set_minor_formatter(dates.DateFormatter('\n\n%b'))

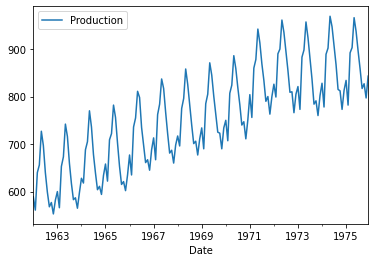

Time Series Dataの可視化

import pandas as pd

pd.read_csv('./UDEMY_TSA_FINAL/Data/monthly_milk_production.csv',encoding='utf8')

title = "Monthly milk production: pounds per cow. Jan '62 - Dec '75"

print(len(df))

print(df.head())

df.info()

df.dtypes

df['Date'] = pd.to_datetime(df['Date'])

df = df.set_index('Date')

df.head()

df.plot()

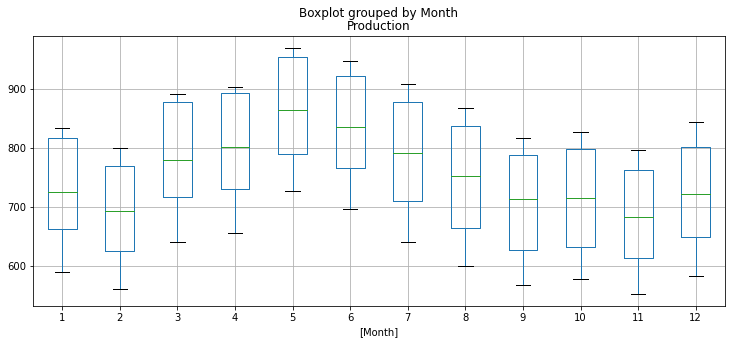

df['Month'] = df.index.month

df.head()

df['Month'].index.strftime('%B')

df.head()

df.boxplot(by='Month',figsize=(12,5))

Boxplot

Time Series Dataの整形/可視化

import numpy as np

import pandas as pd

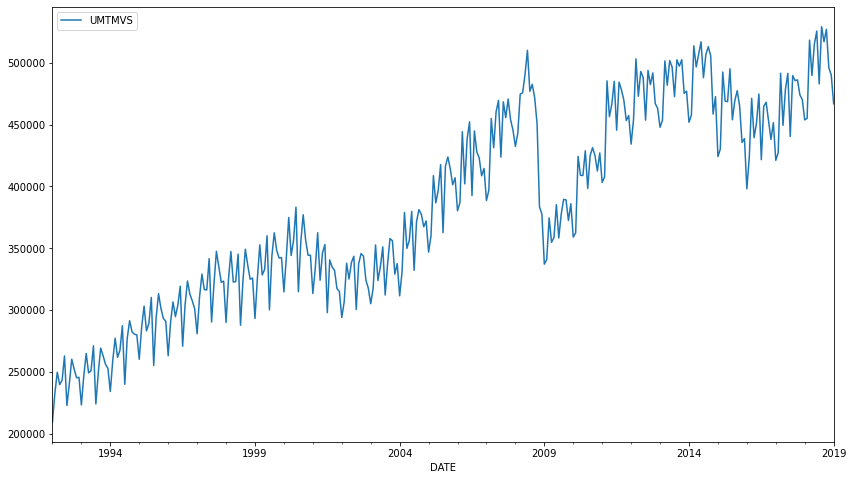

df = pd.read_csv('./UDEMY_TSA_FINAL/Data/UMTMVS.csv')

df.head()

df = df.set_index('DATE')

df.index

df.index = pd.to_datetime(df.index)

df.index

df.plot(figsize=(14,8))

100*(df.loc['2019-01-01'] - df.loc['2009-01-01'])/df.loc['2009-01-01']

df.loc['2005-01-01':].idxmin()

df.sort_values(by='UMTMVS',ascending=False).head(6)

df.loc['2008-01-01'] = df.loc['2009-01-01']

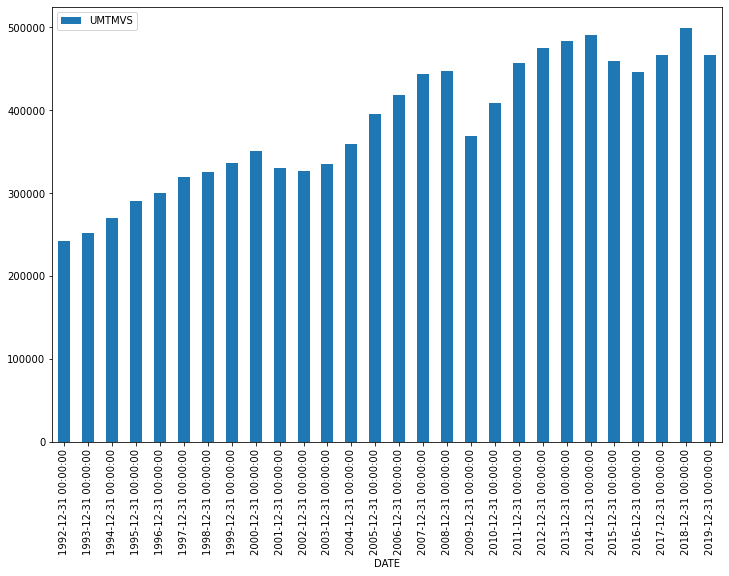

df.resample('Y').mean().plot.bar(figsize=(12,8))

yearly_data = df.resample('Y').mean()

yearly_data_shift = yearly_data.shift(1)

change = yearly_data - yearly_data_shift

change['UMTMVS'].idxmax()

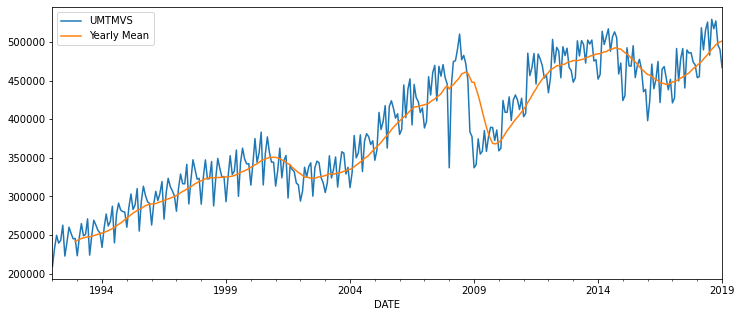

df['Yearly Mean'] = df['UMTMVS'].rolling(window=12).mean()

df.plot(figsize=(12,5))

df = pd.read_csv('./UDEMY_TSA_FINAL/Data/UMTMVS.csv',index_col='DATE',parse_dates=True)

df2008 = df.loc['2008-01-01':'2008-12-01']

df2008.idxmax()

df2008.max()

df_post_peak = df.loc['2008-06-01':]

df_post_peak[df_post_peak>=510081.0].dropna()

len(df.loc['2008-06-01':'2014-03-01'])